Share Rate Carrying out?")

TT Electronics plc (LON:TTG), is not the biggest company out there, but it saw important share value movement during the latest months on the LSE, increasing to highs of UK£2.40 and falling to the lows of UK£1.71. Some share cost actions can give buyers a greater prospect to enter into the inventory, and perhaps purchase at a reduced cost. A question to answer is regardless of whether TT Electronics’ latest investing price of UK£1.71 reflective of the true benefit of the tiny-cap? Or is it now undervalued, supplying us with the prospect to buy? Let us get a glimpse at TT Electronics’s outlook and worth primarily based on the most the latest economic information to see if there are any catalysts for a price change.

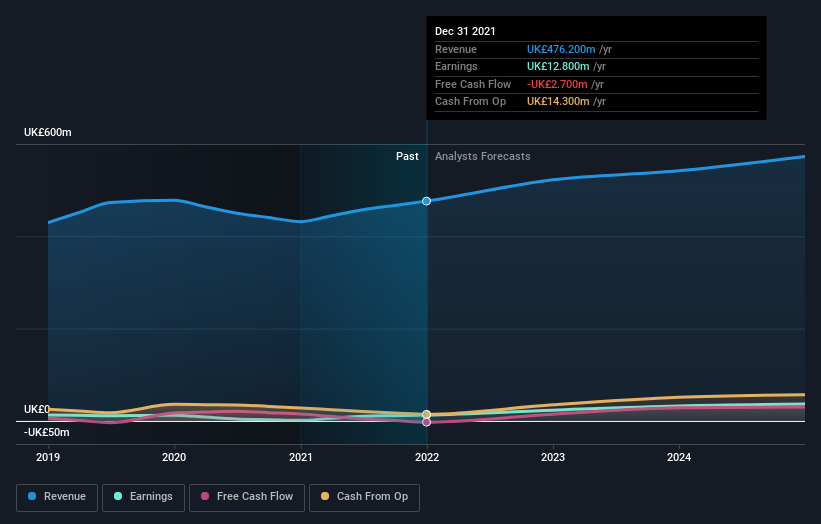

See our latest evaluation for TT Electronics

What is the possibility in TT Electronics?

Superior news, traders! TT Electronics is nevertheless a deal proper now. According to my valuation, the intrinsic price for the inventory is £2.53, which is over what the industry is valuing the company at the minute. This suggests a opportunity possibility to acquire minimal. What is additional appealing is that, TT Electronics’s share price is theoretically quite steady, which could imply two items: to begin with, it may well take the share selling price a when to shift to its intrinsic price, and secondly, there might be fewer likelihood to acquire low in the upcoming as soon as it reaches that value. This is since the stock is much less volatile than the wider current market offered its reduced beta.

Can we hope expansion from TT Electronics?

Long run outlook is an critical component when you are seeking at acquiring a inventory, especially if you are an investor hunting for expansion in your portfolio. Though price traders would argue that it is the intrinsic worth relative to the value that make a difference the most, a additional compelling financial commitment thesis would be high progress prospective at a low cost cost. With revenue envisioned to much more than double in excess of the upcoming couple of many years, the potential seems bright for TT Electronics. It looks like larger hard cash move is on the cards for the stock, which should feed into a better share valuation.

What this implies for you:

Are you a shareholder? Given that TTG is at present undervalued, it could be a excellent time to boost your holdings in the inventory. With a beneficial outlook on the horizon, it seems like this expansion has not still been thoroughly factored into the share price tag. Nevertheless, there are also other components such as capital structure to consider, which could clarify the present-day undervaluation.

Are you a opportunity investor? If you have been maintaining an eye on TTG for a though, now may be the time to make a leap. Its prosperous long run outlook is not thoroughly mirrored in the present-day share value yet, which usually means it is not way