")

Amorn Suriyan/iStock via Getty Images

Methode Electronics, Inc. (NYSE:MEI) has made a notable move by acquiring Nordic Lights. While this acquisition has the potential to influence the company’s direction significantly, I believe certain aspects of MEI’s financial performance in FY 2023 warrant attention. Specifically, the post-acquisition figures indicate a decline in MEI’s EBIT margins and net sales. This raises questions about the integration challenges and the overall efficacy of the acquisition strategy. Furthermore, I find MEI’s capital allocation decisions somewhat perplexing, especially in light of the declining margins. I believe a more cautious approach to cash management would have been advisable. Instead, MEI has adopted a more aggressive stance, leading to decreased cash reserves and an uptick in debt post-acquisition. Based on my valuation model, it appears that MEI’s current valuation is close to being fairly priced. Given these observations and the inherent uncertainties, I would recommend a neutral stance on MEI for now.

Business Overview

Methode Electronics, Inc. (MEI) is a global company that designs and produces mechatronic products, catering to OEMs in sectors like automotive, aerospace, and medical devices. Organized into four segments – Automotive, Industrial, Interface, and Medical – they contribute 54.6%, 39.8%, 5.2%, and 0.4% to the total revenues, respectively. Specifically, the Automotive segment, spearheaded by the Methode Electronics Automotive Group, delivers user interfaces and power solutions, further enhanced by Methode Sensor Technologies’ sensor solutions. Grakon, a key player in the Industrial segment, specializes in custom lighting. The Interface segment boasts brands such as dataMate for data networking and TouchSensor for cutting-edge touch technologies. On the medical front, Dabir Surfaces Inc. innovates in medical device technologies, aiming to elevate patient outcomes.

I believe MEI’s diverse portfolio highlights its adaptability and provides a competitive edge in addressing a wide spectrum of OEM needs. This multifaceted strategy positions MEI for steady revenue inflow from various sectors. However, as I’ll explain, monitoring EBIT margins is crucial, especially in light of recent acquisitions.

Author’s elaboration.

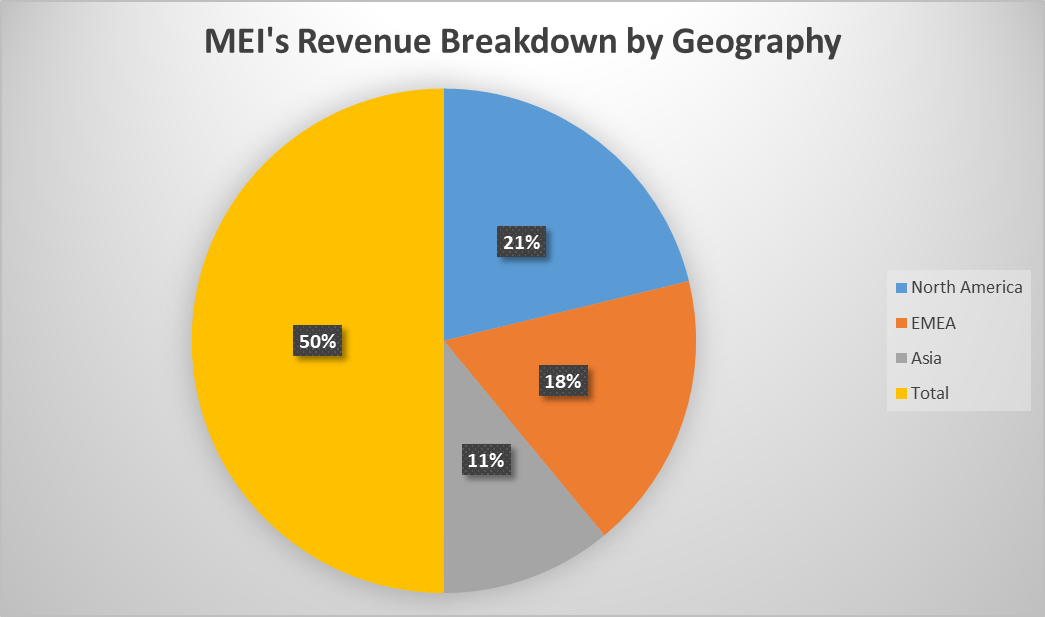

Analyzing the revenue distribution of MEI, it’s evident that the company has a significant market presence in North America, Europe, the Middle East & Africa (EMEA), and Asia. Specifically, North America contributed $122.8 million, EMEA added $103.3 million, and Asia accounted for $63.6 million of the total net sales, totaling $289.7 million. In my view, this distribution suggests that MEI has been successful in its strategic efforts to diversify its market exposure. The acquisition of Nordic Lights Group Corporation further supports this inference, indicating a deliberate move by MEI to expand its geographic footprint. This diversification is crucial as it mitigates risks associated with market concentration and positions the company to tap into emerging opportunities in different regions.

Recent Performance and Post-Acquisition Implications

Indeed, MEI’s acquisition of Nordic Lights Group Corporation is a significant highlight for MEI, enhancing LED lighting solutions, diversifying market exposure, extending its presence in industrial and non-auto transportation markets, and broadening its customer base and geographic reach. This aligns with a recent slight change in revenue distribution over the